Lynne Kiesling

We leave on an intermountain West camping trip Saturday morning, so will be beyond the reach of communication technology for a fair chunk of the next week. But given that the underlying fundamentals have not changed substantially in the past year, even though the prices have, I am re-posting this post, this post, and this post from August, 2005, about gasoline prices. The comments on the original posts were good and plentiful, and I recommend them to you as well.

Aggregate post is below the break. Have a great week!

In KP’s three years of life there’s been a lot of coverage of oil and gasoline markets, and some dominant themes have persisted:

- The unintended consequences of price caps are usually pernicious.

- Environmental regulation, in this case in the form of the EPA federal fuel oxygenate requirement, causes balkanization of regional gasoline markets, causes price differentials across regions, and exacerbates seasonal price spikes.

- The price of oil is one among many factors influencing gasoline prices; environmental regulation is another, as are taxes. Regulation and taxes vary by jurisdiction, causing prices to vary.

- Gasoline prices, like most other retail prices, follow a “rockets and feathers” pattern of response to oil prices. However, just because retail prices are slow to fall when oil prices do, that does not mean that retail gasoline markets are uncompetitive. It’s more a reflection of the inelastic demand for gasoline.

- Part of the reason why the demand for gasoline is inelastic is what I mentioned this morning; fuel is a smaller share of household budgets for most US households.

- Every spring like clockwork, gasoline prices rise for a combination of complex reasons (winter-to-summer fuel switchover, summer driving increase, etc.).

- Every spring like clockwork, Illinois Senator Dick Durbin whinges about “greedy, price-gouging” oil refiners who are sticking it to consumers.

- Every spring like clockwork, the Federal Trade Commission spends a lot of time and effort to investigate the competitive conditions in retail gasoline markets. Every spring like clockwork, they find no evidence of oil refiners’ abilities to influence retail prices in an anticompetitive fashion.

- Right now, high oil prices are being driven by China’s (distorted and subsidized) demand and by risk premia due to uncertainty in the Middle East, Venezuela, and Africa.

- OPEC and its shaky ability to sustain a successful cartel (because of hard-to-detect cheating from smaller members) does not determine world oil prices. OPEC’s decisions influence world oil prices, but they are only one part of a much more complex story, and that complexity is beneficial because it dilutes their ability to withold and raise prices.

- [I saved this for last because it’s the important long-run point] Petroleum is scarce, perhaps even finite, in its supply. Technological change has helped us locate more of it, and pull it out of the ground where we might otherwise not be able to or where it would otherwise have been too costly. That’s the primary reason why prices fell in the 1990s. OPEC’s inability to sustain a cartel exacerbated that price decline. Price increases reflect expectations of future scarcity relative to demand and risk. That is the most powerful mechanism by which we learn both to conserve and to innovate.

[Leaves professor mode, goes downstairs to make herself a well-deserved Manhattan]

OK, here’s the data to show that relative to median household income, gasoline prices have fallen:

Data used to create figure:

- Median household income data for 1980-2000 from Table H-11 of Census historical statistics, in current dollars

- Median household income data for 2001-2003 from Table H-8 of Census statistics from the Current Population Survey, in current dollars.

- Average price of regular unleaded gasoline, 1980-2003, from Table 5.24 of the DOE Annual Energy Review 2004, in current dollars.

GINORMOUS ASSUMPTION MADE: The above graph assumes that the quantity of gasoline consumed per household has been constant over the past 25 years. This is a heroic assumption, but the BLS website was not sufficiently user-friendly to enable me to find data on household spending on gasoline in a useful form, and I desperately want to go downstairs and make that Manhattan!

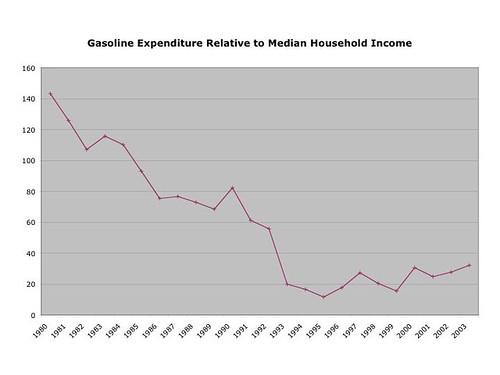

OK, Manhattan in hand … here’s an analysis that improves on the first one. I’ve taken the ratio of [gasoline price x gasoline quantity] to median household income. The gasoline quantity data are from Table 5.13a of the DOE’s Annual Energy Review 2004, in thousands of barrels.

Table 5.13a reports “estimated petroleum consumption, residential and commercial”. That means that I am overstating the amount of residential petroleum consumption, which at least will bias the results in the direction I want; if I’m overstating residential consumption, I’m overstating residential expenditure, so if it declines, then we know that in truth the decline is even larger than depicted. The analysis would be more precise if I could break them out. But here it is anyway:

If anything, this decline is larger than just the ratio of gas price to median household income. Interesting.