[Series header: On the Morning of October 15 the Institute for Energy Research in Washington DC released a report I’d written about the federal government’s wind power cost estimates. (Links available here.) Later that day Michael Goggin of the American Wind Energy Association, the lobbying organization in Washington DC that represents the wind energy industry, posted a response on the AWEA website: “Fact check: Fossil-funded think tank strikes out on cost of wind.” I’m considering points made by the AWEA response in a series of posts.]

Goggin objects to my report’s emphasis on the high cost of wind energy. He said, “The reality is that wind energy is driving electricity prices down, thanks to large recent reductions in its cost.” I agree with Goggin, as I said earlier in this series of replies, at least on price suppression: “Wind power is responsible from bringing down average prices in regional power markets, a consequence of subsidizing entry of generation with high capital costs but low marginal operating costs.”

But the effect of wind energy on prices is only obviously negative in the short run. Longer term the cost of energy could rise. More importantly, the price suppression effect is only tangentially related to the overall benefits and costs of wind power policy and so of only modest policy relevance.

The basic short-run “price suppression” effect is explained various places–here is a bit from a short report produced by the staff of the Public Utilities Commission of Ohio, “Renewable resources and wholesale price suppression” (August 2013):

Price suppression is a widely recognized phenomenon by which renewable resources produce lower wholesale market clearing prices. The economic theory that drives price suppression is actually quite simple. Renewable resources such as solar and wind are essentially zero marginal cost generators, as their “fuel” costs (sunlight and wind) are free. As such, they will always be dispatched first by the grid operator, thereby displacing units with higher operating costs. This results in lower wholesale market clearing prices than would have been experienced in the absence of the renewable resources.

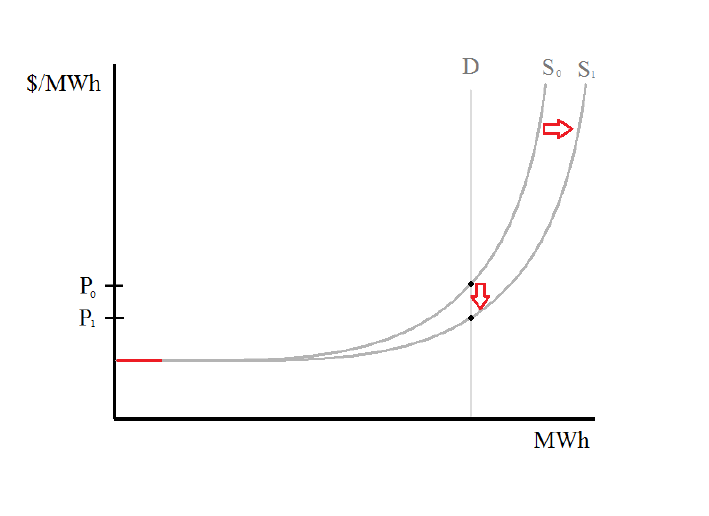

A simple graphical representation appears below. The new renewable resources (depicted by the red line) are added to the dispatch stack, shifting the supply curve out and to the right. This results in a lower cost unit setting the market clearing price, shifting the equilibrium price down from Po to P1.

The above analysis, so far as it goes, adequately shows the simple short-run impact of adding low marginal cost resources to a supply curve. The marginal cost of producing wind energy isn’t zero–wind turbines experience wear from operation and non-zero maintenance costs. But the marginal costs are low relative to most other power plants and the short-run impact on spot prices is to push prices down. In the simulations for Ohio analyzed by the PUCO staff, the effect is a price suppression of between $0.05 and $0.20 per MWh (or, to put it in residential consumer terms, a reduction in energy cost of 0.02 cents per kwh).

But, as the staff of the Public Utilities Commission explain in their report, observing a tiny tiny price suppression effect doesn’t indicate anything about overall costs and benefits or about least-cost capacity expansion. The above analysis is a short-run assessment that ignores longer term effects on investments and retirement of assets. A more complete assessment, they said, would need “to consider additional variables such as capital and capacity costs, renewable energy credit (REC) prices, and transmission upgrade expenses.”

And that is among the problems with Goggin’s simple-minded trumpeting of a price suppression effect as some sort of renewable energy triumph: it ignores the future consequences of the policy. Other things being equal, as intermittent low-marginal-cost resources are added to a power system, less-flexible medium-low marginal cost baseload power plants tend to be most disadvantaged and most likely to be retired. At the same time, the resulting increased need for flexible, dispatchable resources will tend to support investment in responsive natural gas generators that have lower capital costs but medium to high marginal costs.

These changes to the generation portfolio in a market will also shift the shape of the supply curve. It is an empirical question, or will be in five or ten years when energy markets have finished adjusting to the 2018-2013 wind energy construction boom in the United States and data is available, whether the overall effect has been to reduce or increase average prices to consumers.

But there is at least on more point: public policy analysis ought to involve a careful counting of projected benefits and costs. It is hardly surprising that subsidizing entry of production capacity would tend to drive down market prices in the short run, but that says nothing about either the short-run or long-run overall benefits and costs of the subsidy policy. The high capital costs of wind energy are one big signal that the steel, concrete, rare earth magnets, other component parts and manufacturing expertise that are drawn into wind energy production all have valuable potential other uses in the economy. We forgo these other potential contributions when policy steers these resource into electric power generation.

Are consumers better off when public policy pulls some of these resources from the manufacture of other goods and services and pushes these resources into electric energy supply? Maybe yes and maybe no, but the price suppression effect is mostly about the division of the spoils of wind power policy, and has little to do with the overall benefits and costs of the policy.